Why there is no better investment than Spanish real estate

6 May 2021

Even though the income from a savings account does not even earn you the salt on your French fries, we Belgians are all saving like crazy. Are there no better uses for your money than to watch it shrivel up on the spot? Yes, an investment in Spanish property is the best thing you can do with a pot of extra cash.According to our calculations, it brings up to 66 times more than a savings book!

Saving in a savings account = impoverishing every day

Belgians are notorious hoarders. There is a huge amount of money in our current and savings accounts. At the end of February, we collectively had 297 billion euros parked in our savings books. By comparison, in 2000 it was 94 billion euros. Our current accounts hold even more: 304 billion euros in total. However, those savings in the bank barely bring in a pink penny. Five years ago, market leader BNP cut interest rates on savings books to the legal minimum: 0.11 percent. Other banks followed suit. What moochers first described as a temporary phenomenon now appears to be the new normal. For those of you whose heads were on the table in math class, that means that every hundred euros in your savings account will earn you 11 cents annually. You won't even buy a pack of gum with that. But it could be worse. Recently, ING started charging a punitive interest rate of 0.5 percent for those with more than 250,000 euros in their accounts. You are paying, in other words, to put your money in the bank. Even for a bank, all this savings behavior is too much. ING is also changing the rates for popular account packages. The Lion Account, previously free, now costs $1.90 per month. But, you reason, money in a savings account is an apple of your eye, isn't it? Bwa, that apple shrivels by the day anyway. Inflation causes your savings to be worth a little less every day. Anyone who puts 1000 euros in a savings account today will have 1006 euros, the full six euros, saved by 2026. But for a shopping cart worth 1,000 euros, you will pay 1,074 euros in five years. There is no prospect of higher interest rates, while inflation does continue to fester. In March, it even doubled.Money in the savings account as an apple for the thirst? That apple shrivels by the day.

Why it's important that your savings pay off

Those who retire at 67 have (hopefully) many years ahead of them. Currently, life expectancy shoots above 80 years. The problem: during your career you have been earning more and more, but then suddenly you fall back on a meager pension. While you need more money in your old age. Because finally you have time for terraces, city trips and a big stack of pancakes at the local coffee house. And all those adorable grandchildren, of course, also pass by regularly with an open hand. [caption id="attachment_12675" align="aligncenter" width="2560"] All the things you never had time for before....[/caption]

And those who become needy - we don't wish it on you - had better have some money in surplus, too. Residential care centers cost pieces of people. That is the great paradox: just when you could use a few extra bucks, you have to make do with a lot less.

All the things you never had time for before....[/caption]

And those who become needy - we don't wish it on you - had better have some money in surplus, too. Residential care centers cost pieces of people. That is the great paradox: just when you could use a few extra bucks, you have to make do with a lot less.

After age 67, you fall back on a meager pension. While you want to spend more in your old age.The challenge is to at least partially fill the gap between your last paycheck and your retirement. To create a recurring extra income, a virtual money machine from which you can tap a few flaps each month. So that you can maintain your purchasing power even after retirement. No one is going to do it for you. It is your responsibility. And it's best to think about it during your career. Before it's too late.

Alternatives to the savings book

We learned earlier that the interest rate on your savings will not do. For an extra 500 euros per month, you need a capital of almost 5.5 million euros in the bank. That, unless your name is Marc Coucke, is unrealistic. But how can it be done?1/ Eating up wealth

Of course, after your 67, you can live as if it could be done at any time. Then it may not seem excessive to plunder your savings book. Suppose you withdraw an additional 500 euros every month. A savings account of 200,000 will then be worth only 100,000 after 10 years, inflation permitting. Then you will be 77 years old and, with any luck, you will have 20 more years ahead of you. Chances are then that you will be in the black in no time.2/ Savings Insurance

Switching to branch-21 products then? You can, but realize that you are losing purchasing power in this way. The guaranteed interest rate is low, less than 0.5 percent gross. Much more than that savings book is not. Profit sharing also rarely exceeds 1 percent gross. Add to that the heavy entry fees, sometimes as high as six percent, and the fact that you are tying up your money for at least eight years, and you know that savings insurance is not the best choice.3/ Shares and funds

Stocks and funds potentially bring in more than savings insurance, but you also take on more risk. There is a chance that such funds will fall quickly and hard. Even shares of companies that meet the highest quality standards do not provide security. Just ask the duped shareholders of the late Fortis. Mixed funds, which include bonds in their portfolio, are more defensive. However, this does not mean that they are risk-free. Such funds are sensitive to rising inflation. During corona, they fell as much as 20 percent. You'd rather save yourself that stress.4/ Gold

Of course, you can convert your capital into gold. Being a gold owner, it even sounds cool. But again, you have no fixed interest income. Moreover, the performance is mainly related to real interest rates in the US. Substantial fluctuations there put your yields on the line. Compared to last summer, for example, the gold price now clocks in at a 15 percent loss. No, it's not good for peace of mind. [caption id="attachment_12672" align="aligncenter" width="2560"] Cool it is, though.[/caption]

Cool it is, though.[/caption]

The benefits of investing in rentable Spanish property

Compared to all of the above, an investment in Spanish real estate is an extremely safe choice. You guarantee yourself a return on investment that leaves the other options far behind. The rest are not in the finish photo. And here's why:Flexibility

A country house on the Spanish costas fulfills two needs: you earn money from it and you can enjoy it yourself. And you would be crazy not to do the latter. On the southern coasts of Spain, the sun shines almost all the time. The beaches are beautiful, the cuisine is finger-licking good, and the climate the most salubrious in the world. You can stay there yourself as often as you like. If you're not there, you'll see the returns tick up. Flexibility also means: the possibility of temporarily putting the house into an annual rental, for example because you are very busy at work. You also determine the periods in which you rent (weekends, mid-weeks, weeks, winter rentals).Rental prices are not limited

If you rent out a property in Belgium under the 3-6-9 system, you can't just jack up the rent substantially. You are limited to the little latitude the health index allows you. Vacation rentals, on a short-term basis, are not subject to those rules at all. If inflation skyrockets, you can adjust the rent accordingly. Is the region suddenly gaining popularity? Is that new starred restaurant in the neighborhood creating more demand? Raise, that rent! You are not accountable to anyone.

More certainty

Short-term rentals mean a smaller chance of damage and - in proportion to the length of stay - a larger guarantee.High rental prices

During the vacation periods, demand for vacation homes on the Spanish costas skyrockets. Consequence: you can charge high rental rates.No worries with rental service

You don't have to not receive every vacationer and provide them with clean towels. That's what a rental service takes care of. This comes at a price, but the benefits far outweigh it. A rental service department cleans, checks contents, does minor repairs, hands over keys, answers tenant questions, and provides linens and towels. You make money while you sit back.How much does an investment in Spanish real estate yield?

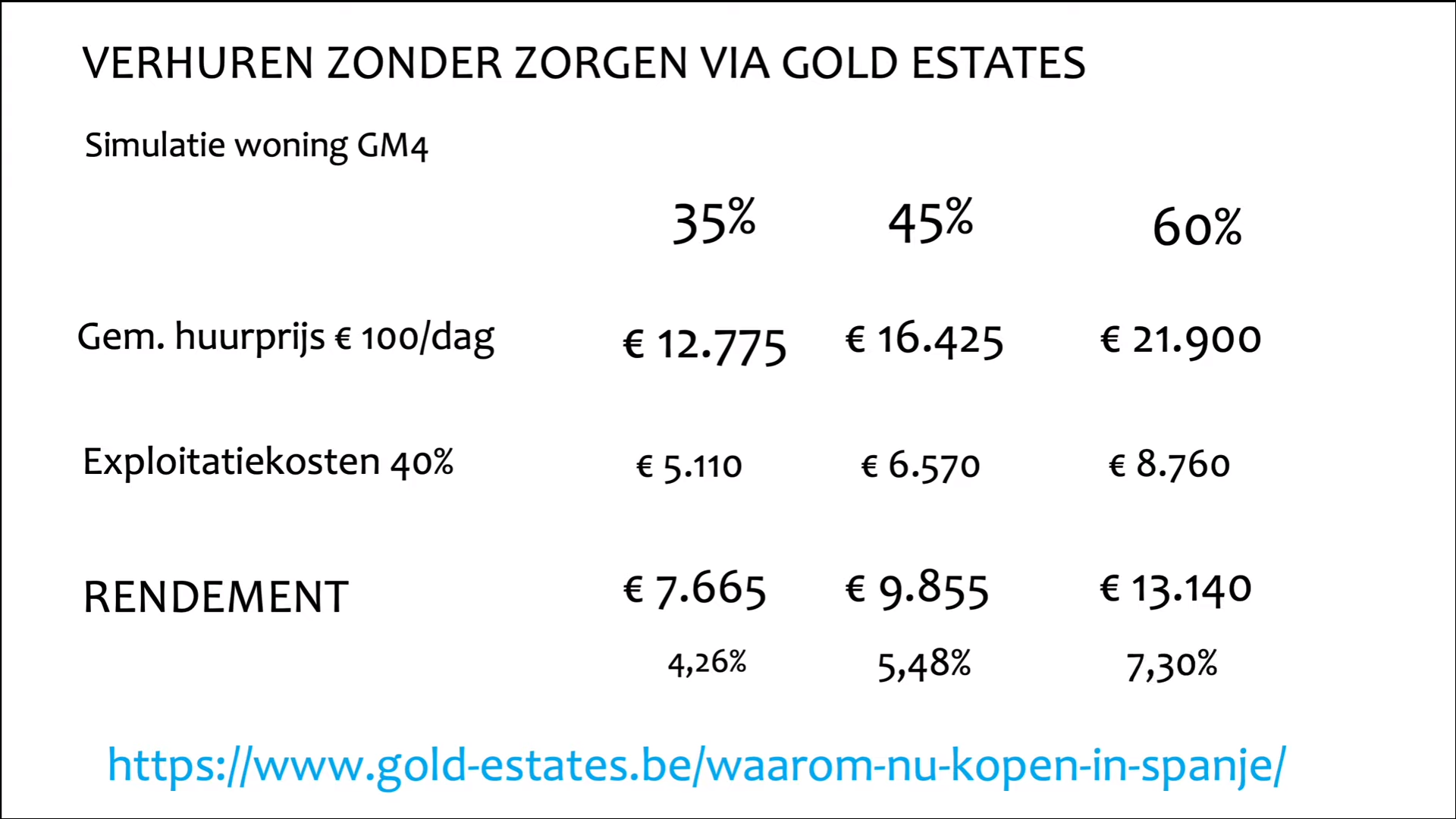

Of course, much depends on the location, the condition of your property and the time period. Vacationers prefer to stay in new buildings, equipped with all modern facilities and not too far from the coast. Gold Estates expert Gunther Van de Walle created the simulation below for a property in Gran Mirador IV, a new development in Mutxamel of which there are still a few last units available: Those who want to listen to Gunther's detailed explanation can watch this webinar. The section on rental yield begins at 1:20:52.

The average rent is conservatively estimated, the cost of operation generous. This projection is therefore rather conservative, but it immediately becomes clear that a vacation home in Spain potentially yields more than a 3-6-9 rental of a residence in Belgium. And you can sit on your own in the sun from time to time, which cannot be said of a rented house in your own country.

Compare with the interest rate on a savings account - 0.11 percent, remember? - is not at all fair: at 60 percent occupancy, an investment in Spanish real estate yields 66 (sixty-six!) times more.

Who is going to let their money rot in a savings account?

Those who want to listen to Gunther's detailed explanation can watch this webinar. The section on rental yield begins at 1:20:52.

The average rent is conservatively estimated, the cost of operation generous. This projection is therefore rather conservative, but it immediately becomes clear that a vacation home in Spain potentially yields more than a 3-6-9 rental of a residence in Belgium. And you can sit on your own in the sun from time to time, which cannot be said of a rented house in your own country.

Compare with the interest rate on a savings account - 0.11 percent, remember? - is not at all fair: at 60 percent occupancy, an investment in Spanish real estate yields 66 (sixty-six!) times more.

Who is going to let their money rot in a savings account?